I looked at stocks, time deposits, bonds, and crypto before I chose MP2. Stocks were too volatile. Time deposits were too safe in the wrong way — the returns barely moved. Crypto was a gamble I wasn’t ready for.

MP2 was different. Government-backed, tax-free dividends, and returns that consistently beat bank products. That combination made the choice clear.

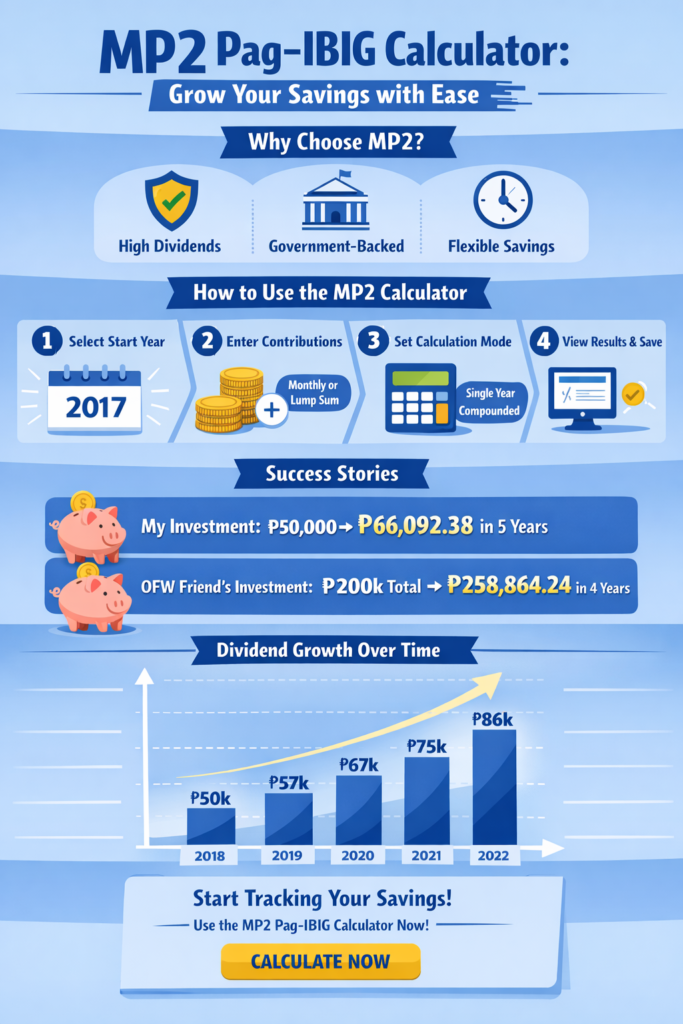

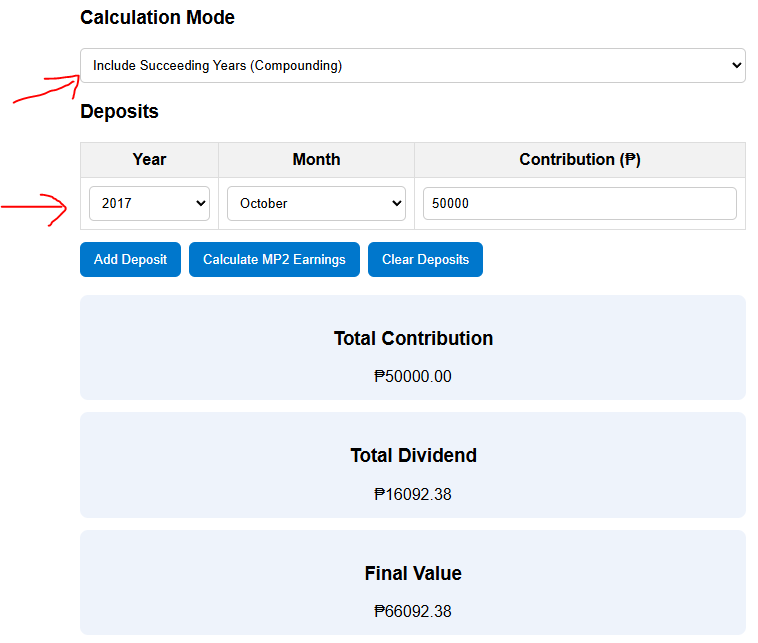

I deposited ₱50,000 in October 2017. At maturity in 2021, I walked away with ₱66,092.38 — ₱16,092.38 tax-free, zero stress. But I almost didn’t get the most out of it because I didn’t plan properly at the start. Use the calculator below before you commit to any amount.

What is MP2 and why does it beat most savings options?

MP2 (Modified Pag-IBIG II) is a voluntary savings program from Pag-IBIG Fund. It pays annual dividends, protects your principal with full government backing, and charges zero tax on your earnings.

| Savings option | Average return | Tax on earnings | Risk |

|---|---|---|---|

| Regular savings account | 0.1–0.5% | 20% final tax | None |

| Time deposit | 1–3% | 20% final tax | None |

| MP2 savings | 6–7% | None | None |

| Stocks | Varies | Capital gains | High |

After comparing all of them, I kept coming back to one fact: MP2 dividends are completely tax-free. Everything you earn is yours. Compare that to a time deposit where 20% of your return goes straight to withholding tax. The gap adds up fast.

How to use the MP2 Pag-IBIG savings calculator

The MP2 savings calculator estimates your total return based on contribution amount, deposit frequency, and your chosen dividend option. Enter your numbers, pick annual payout or compounding, and the tool shows a full 5-year projection.

Here is what each field means:

- Monthly contribution — how much you deposit each month. Minimum is ₱500.

- Lump sum or one-time deposit — for a single large contribution or irregular deposits

- Dividend option — annual payout sends dividends to your account each year; compounding reinvests them

- Dividend rate — use the current declared rate or the historical average for long-term projections

The guide image above shows exactly what to enter and where. Even if you are not comfortable with financial calculators, it walks through every field step by step.

If you have not enrolled in MP2 yet, read the full guide on how to open an MP2 account first before running the calculator.

Annual dividend payout vs. dividend compounding: which should you pick?

Dividend compounding reinvests your earnings back into your balance. Your next cycle earns dividends on a larger amount. Annual payout sends dividends to your account each year — useful if you need the cash flow now.

| Option | Best for | Outcome |

|---|---|---|

| Annual payout | Need yearly income | Lower total at maturity |

| Compounding | Maximum growth | Higher total at maturity |

I chose compounding without hesitation. When dividends compound, your money earns on itself year after year. The longer you hold, the bigger the gap between the two options.

The only downside is the 5-year wait. You will not touch that money until maturity. If you need liquidity, annual payout makes more sense. If you can leave it alone, compounding wins every time.

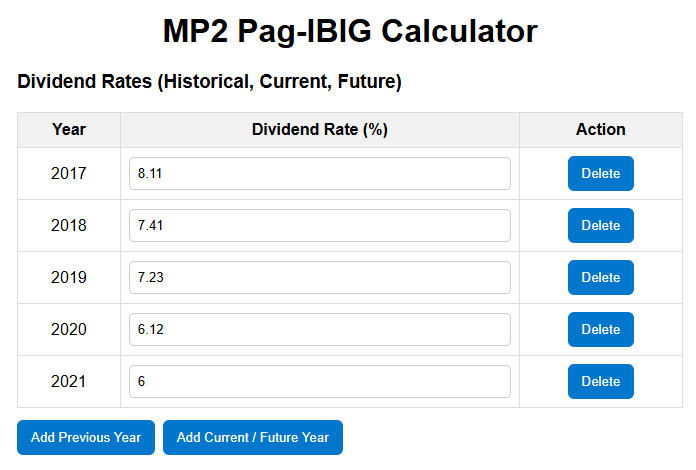

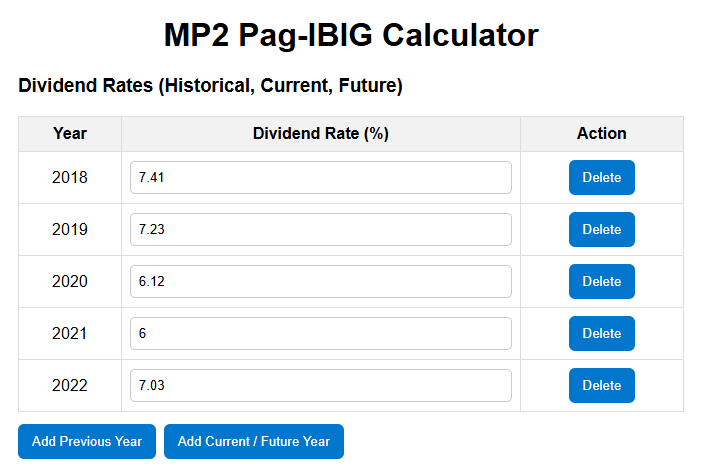

MP2 dividend rates from 2011 to 2025

Pag-IBIG declares the MP2 dividend rate annually based on fund performance. The rate is not fixed — but over 15 years, it has consistently outperformed savings accounts and time deposits.

| Year | MP2 dividend rate |

|---|---|

| 2011 | 7.59% |

| 2012 | 6.23% |

| 2013 | 7.36% |

| 2014 | 4.58% |

| 2015 | 8.11% |

| 2016 | 7.26% |

| 2017 | 7.41% |

| 2018 | 7.41% |

| 2019 | 7.23% |

| 2020 | 6.12% |

| 2021 | 6.00% |

| 2022 | 6.00% |

| 2023 | 7.03% |

| 2024 | 7.12% |

| 2025 | 7.17% |

The 2021 and 2022 dip to 6.00% happened during the pandemic. Banks were offering under 2% on time deposits at the same time — and that 2% was still taxed at 20%. A tax-free 6% return during a global economic downturn was a strong result, not a disappointment.

When people tell me they’re hesitant because the rate isn’t fixed, I tell them to compare it against everything else available at the same time. The 5-year average tells a better story than any single year.

Real examples: what your money actually earns in 5 years

My account

I deposited ₱50,000 in October 2017 and chose dividend compounding. No additional deposits — I left it alone for 5 years. At maturity in 2021, the total was ₱66,092.38. That’s ₱16,092.38 in tax-free earnings.

No forms to file. No withholding to track. The full amount landed in my account at maturity.

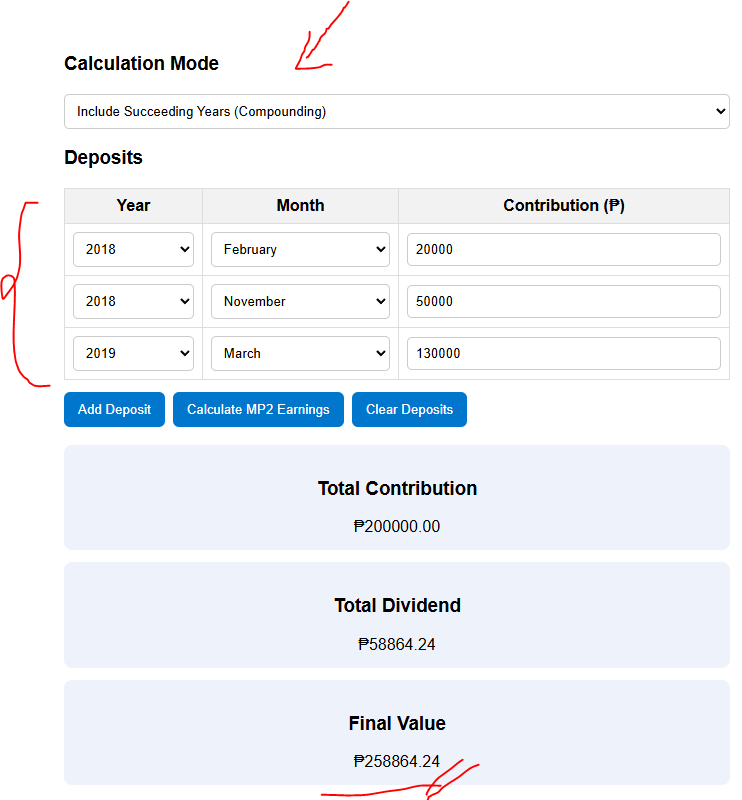

An OFW friend’s account

A friend working abroad made three deposits: ₱20,000 in February 2018, ₱50,000 in November 2018, and ₱130,000 in March 2019. Total invested: ₱200,000. At maturity in 2022, the payout was ₱258,864.24 — a gain of ₱58,864.24.

When he saw that number, he wanted to re-invest immediately. That’s why I built these guides. Once you see the actual results, the hesitation disappears. More Filipinos — especially OFWs — should be putting their savings here.

The staggered account strategy for steady income

You can open more than one MP2 account. Most people don’t realize this. I started with one, then opened additional accounts about 6 to 12 months apart, depositing a lump sum into each.

When you stagger the opening dates, each account matures at a different time. Instead of one big payout every 5 years, you get regular payouts on a rolling cycle. MP2 becomes something closer to a passive income stream.

Set it up early, and the payouts become predictable. Ten minutes of planning, years of consistent returns. Pair it with low-maintenance options like digital banking tools like the DiskarTech card to keep accessible funds separate from your MP2 nest egg.

Is MP2 worth it if you only have ₱500 a month?

Yes. Start with ₱500. The return on that amount is modest — but the real value is what you learn. You see exactly how the contribution schedule works, how dividends accumulate, and what the payout process looks like at maturity. That knowledge is what pushes you to scale up later.

With the rising cost of living in the Philippines, every peso that earns a return matters. ₱500 in MP2 beats ₱500 sitting in a savings account at 0.25% per year — with zero tax eating into the difference.

MP2 dividends are also completely exempt from income tax. Nothing to declare, nothing to withhold. Your full return stays in your pocket, and it won’t complicate your annual ITR filing either.

Frequently asked questions about the MP2 Pag-IBIG savings calculator

- What is the MP2 Pag-IBIG savings calculator?

- It is a tool that estimates your total return over 5 years based on your contribution amount, frequency, and dividend option. Use it to plan how much to invest before you commit.

- What is the minimum amount to invest in MP2?

- The minimum contribution is ₱500. There is no maximum. You can start small and add to your account anytime.

- Is the MP2 dividend rate fixed every year?

- No. Pag-IBIG declares the rate annually based on fund performance. Since 2011, it has ranged from 4.58% to 8.11%.

- What is the difference between annual dividend payout and dividend compounding in MP2?

- Annual payout credits your dividends to your account each year. Compounding reinvests them so they earn more dividends in the next cycle. Compounding gives a higher total at maturity.

- Can I open multiple MP2 accounts?

- Yes. Opening accounts 6 to 12 months apart is a smart strategy. Each account matures separately, giving you a regular payout cycle instead of one lump sum every 5 years.

Comments 3