A family friend brought her recent payslips to show me. She teaches public high school in Angeles. Veteran teacher, fifteen-plus years of service.

After I looked at the numbers, I understood why she seemed so tired.

She earns ₱33,705 a month. She takes home ₱5,008.92.

That ₱5,000 is not a lifestyle choice. It is the legal floor written into the General Appropriations Act to ensure government employees retain at least a survival baseline after every automatic deduction. And loans for teachers in the Philippines have become so normalized by 2026 that a clean payslip, one without four or five private lender codes printed across it, is considered unusual in most faculty rooms.

This post breaks down how that happened, who profits from it, and what a newly licensed teacher can do before the loan machine finds them.

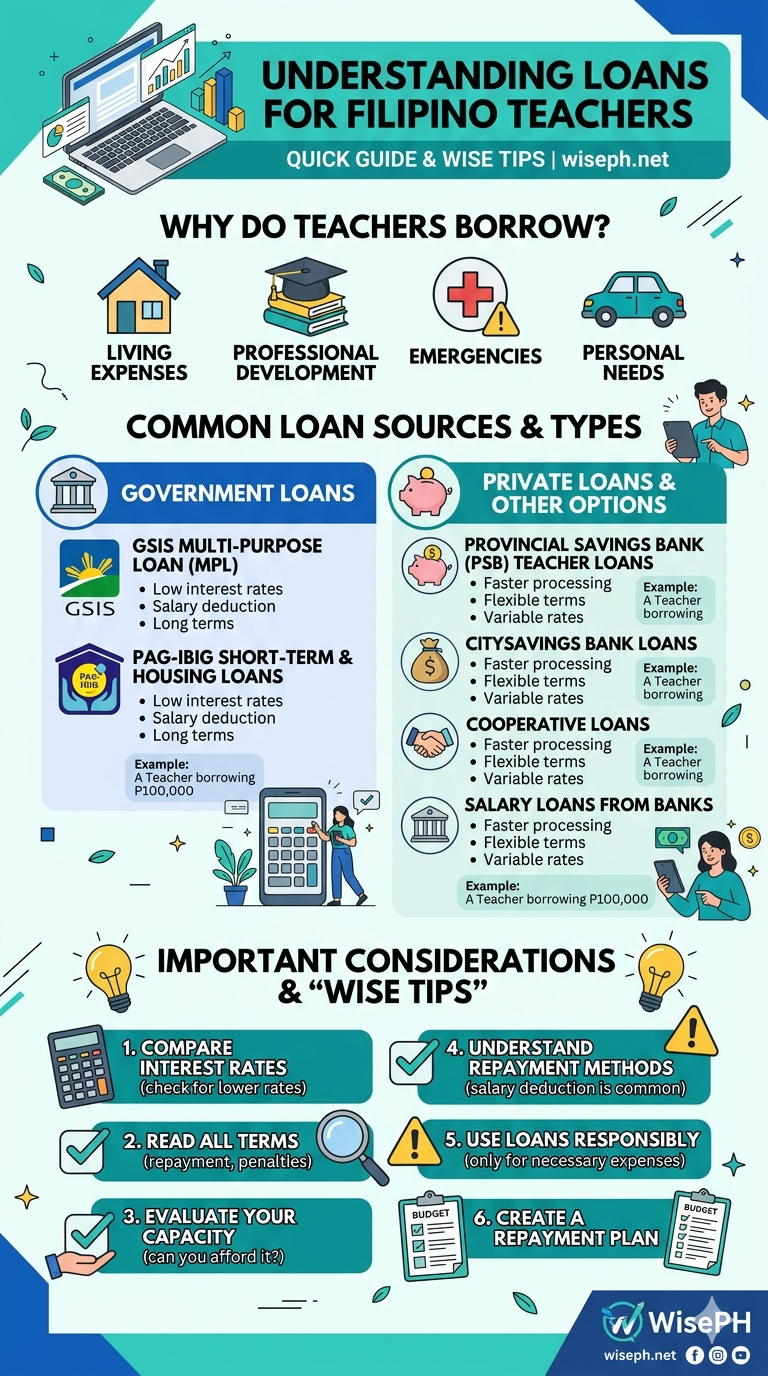

Why do DepEd teachers end up drowning in debt?

Teachers borrow because their salaries do not cover the actual cost of being a teacher. School budgets rarely fund classroom supplies, digital tools, or family emergencies. When the money runs out, the loan forms are already waiting in the faculty room. As a result, loans for teachers are not a fringe product; they are the default financial tool of the Philippine public school system.

Three structural forces drive the cycle, and none of them is fixable with a budgeting seminar.

First, there are unfunded mandates. DepEd’s 2026 “Smart Classroom” directive requires laptops, heavy-duty printers, and mesh routers in every classroom. Most schools cannot supply them through their official budgets. So teachers buy them on personal credit, paying interest on what is essentially a government infrastructure expense.

Second, a salary that sits below the actual cost of living. A Teacher I earns ₱31,705 basic pay under Salary Grade 11, Step 1, the third tranche of EO 64’s Salary Standardization Law. In a city like Angeles, a family of four needs close to ₱40,000 a month just to get by, based on current inflation and the rising cost of living in the Philippines in 2026. The math does not balance without borrowing.

Third, the social architecture of the faculty room. Lending agents, often called “Liaison Officers,” are sometimes fellow teachers who earn referral commissions for every new loan they facilitate. Borrowing is treated as normal. Saying no is what makes you stand out.

How the APDS turns your salary into a collection machine

The Automatic Payroll Deduction System (APDS) is what makes loans for teachers so attractive to private lending institutions. Every accredited lender gets a four-digit payroll code: City Savings Bank uses 0339, BDO Network Bank uses 0918, East West Rural Bank uses 1010. Once that code is on your payslip, the monthly payment is extracted before your salary ever reaches your bank account.

For lenders, teachers are close to the ideal borrower: government employee, stable lifetime income, mechanical repayment, and near-zero default risk as long as the teacher stays employed.

The legal constraint is the Net Take-Home Pay (NTHP) floor: under the General Appropriations Act, no DepEd employee’s take-home pay can fall below ₱5,000. DepEd’s central payroll software blocks any new deduction that would breach that floor.

In theory, that is a protection. In practice, it functions as a marker for how much room the next lender can still claim. Understanding why your SSS contributions matter as a government employee is important, but for DepEd teachers, the more pressing education is learning how APDS codes silently consume a payslip from the inside out.

The four stages of the teacher debt spiral

This happened to someone I know personally, in Angeles, over several years. The progression of loans for teachers follows the same four-stage pattern nearly every time.

Stage 1: The classroom subsidy

It starts small and well-intentioned. Chalk allowances run dry mid-semester. Printing materials cost more than the school budget covers. A teacher takes a ₱10,000 personal loan to keep the classroom functional. It feels like a sacrifice, not a trap.

Stage 2: The co-maker trap

Filipino teacher culture is communal. A colleague has a medical emergency and needs a fast-cash loan. The teacher signs as co-maker as a personal favor. A year later, the colleague defaults. The outstanding balance transfers automatically to the co-maker’s payslip. She is now paying a stranger’s debt with no warning and no legal recourse.

Stage 3: The consolidation illusion

With two or three APDS deductions running, the payslip gets tight. A private lending institution (PLI) offers to consolidate everything into one “manageable” monthly payment. Approval is fast. The forms are smooth. But the fine print resets the loan term to Year 1. The effective interest rate, once the 6% upfront service charge and documentary fees are added, lands between 15% and 22%. A teacher three years into a five-year loan is now starting over.

Stage 4: The shadow economy

The payslip hits the ₱5,000 legal floor. No new official deductions can be added. But the need for cash does not stop. Teachers enter the shadow market: “5-6” lenders operating entirely outside the APDS, charging rates that make City Savings look conservative. The official payroll system was supposed to be a safeguard. Instead, it becomes the entry point to something far less regulated.

What a Teacher I actually takes home in 2026

Under EO 64’s third salary tranche, a Teacher I earns ₱33,705 gross per month including the ₱2,000 PERA allowance. After statutory deductions and a typical loan load, the actual take-home pay is ₱5,008.92, the legal minimum. In Angeles or any major city in 2026, that amount does not cover a week of decent meals and transportation for a family.

Here is the exact breakdown from payslips I reviewed this year:

| Gross income | Amount |

|---|---|

| Basic salary (SG 11, Step 1) | ₱31,705.00 |

| PERA allowance | ₱2,000.00 |

| Gross total | ₱33,705.00 |

| Mandatory deductions | Amount |

|---|---|

| GSIS (9% personal share) | ₱2,853.45 |

| PhilHealth (2.5% employee share) | ₱792.63 |

| Pag-IBIG | ₱200.00 |

| Withholding tax (estimated) | ₱1,850.00 |

| Subtotal | ₱5,696.08 |

Clean net after statutory deductions: ₱28,008.92

| Loan deductions (typical trapped teacher) | Monthly amount |

|---|---|

| GSIS Multi-Purpose Loan | ₱3,500.00 |

| Pag-IBIG Multi-Purpose Loan | ₱1,200.00 |

| PLI 1 (e.g., City Savings Bank / BDO Network) | ₱8,500.00 |

| PLI 2 (digitalization / laptop loan) | ₱5,800.00 |

| PLI 3 (consolidation loan) | ₱4,000.00 |

| Total loan deductions | ₱23,000.00 |

Final take-home pay: ₱5,008.92

In short, this is what loans for teachers in the Philippines actually look like behind the payslip. Not a credit card. Not a personal choice. A structured deduction system that consumes 85% of gross income before the teacher touches a peso.

That PLI 2 line is a laptop loan. Specifically, a mid-range unit meeting 2026 “Smart Classroom” specs costs ₱42,000 to ₱48,000. On a 12-month PLI plan, that adds roughly ₱4,500 per month in payments, for a device the government mandate required and the school budget did not cover.

Three ways lenders bypass the ₱5,000 floor

The NTHP floor is enforced by DepEd’s payroll software. In theory, no new APDS deduction is supposed to push a teacher below ₱5,000. Nevertheless, lenders have engineered three workarounds that keep loans for teachers growing even after the official payroll limit is reached.

The queuing mechanism. A PLI approves a new loan even when a teacher’s payslip is already at the legal minimum. Instead of activating the deduction immediately, the lender queues it. The month any older loan finishes paying off, the queued deduction activates automatically to fill the vacancy. No relief arrives. The payslip simply swaps one creditor for another.

ATM card pawning (“Sangla”). Because lenders cannot legally extract more through the official payroll, they target the bank account directly. A lender requires the teacher to surrender their government payroll ATM card and PIN as collateral. On payday, an agent withdraws the full deposit at an ATM, takes the month’s cut, and returns whatever is left. The ₱5,000 legal floor evaporates the moment it clears the payroll system.

Post-dated checks and legal coercion. Some PLIs require teachers to issue a stack of post-dated checks covering amounts beyond what the payslip system allows. If a teacher misses a manual deposit, the lender threatens a BP 22 (Bouncing Checks Law) case or files an administrative complaint with DepEd. For a public school teacher, an administrative complaint can jeopardize their PRC license. That one threat is usually enough to force payment by any means.

How debt locks teachers into jobs they want to leave

Leaving DepEd while carrying active loans for teachers is financially catastrophic. The moment a teacher resigns, automatic payroll deductions stop, but the loan balances do not. Specifically, most PLI contracts include a clause making the full outstanding balance due and demandable upon separation from service.

This creates what I have heard called “deduction lock-in” among teachers in Pampanga, and it plays out in four specific ways.

First, terminal leave pay gets absorbed. Teachers count on accumulated leave credits as a transition fund when they resign. However, GSIS and accredited PLIs can legally offset outstanding balances against that final payout. Cases this year show teachers who resigned after ten years of service expecting ₱150,000 in terminal leave, and received a check for zero.

Second, promotions stop making financial sense. A ₱3,000 raise from a Master Teacher appointment sounds meaningful on paper. But queued loans waiting in the APDS absorb that increase automatically on the first payroll cycle. More responsibility, higher stress, and zero increase in daily take-home pay. As a result, the incentive to grow professionally disappears.

Third, the 2026 restructuring programs extend the lock-in rather than end it. Consolidation lowers the monthly amortization but resets the loan term. Specifically, a teacher two years from debt freedom might sign a program that stretches the obligation by another five years, anchoring them to their DepEd post until 2031 just to keep the APDS running smoothly.

Finally, even migration is gated. POEA/DMW processing for overseas teaching placements often requires a settled arrangement with government creditors like GSIS. For many teachers, the only realistic path out is to stay in, working a job they have outgrown, just to satisfy an automated deduction system.

What the government is doing in 2026, and what’s still missing

Three measures are currently in place. However, none of them addresses the salary gap that makes borrowing a mathematical certainty for most teachers.

| Policy | What it does | Verdict |

|---|---|---|

| GSIS Consolidation Program (Angara, April 2026) | Moves teachers from high-interest PLIs to GSIS at lower rates | Trap: resets the loan term, extends debt by 3 to 5 years |

| Two-loan APDS cap (TCAA 2026) | Limits PLI access to two regular deductions per payslip | Bandage: stops the queue officially, not shadow lenders |

| MOOE augmentation (2026 GAA) | Funds digitalization through school revolving funds | Partial fix: only works if money clears the division office |

| ₱50,000 salary bill (ACT Teachers) | Replaces SG 11 with a living-wage-level basic pay | Root cause fix: stalled in Congress on fiscal space grounds |

| RA 11997 (Kabalikat sa Pagtuturo Act) | ₱10,000 teaching allowance for SY 2025-2026 | Insufficient: one-time allowance against ₱40,000-plus annual borrowing need |

Specifically, the ACT Teachers’ ₱50,000 salary bill is the only proposal targeting the root cause. As long as a Teacher I earns ₱31,705 basic pay while the family living wage in cities like Angeles has climbed toward ₱40,000, loans for teachers will remain a structural necessity, not a personal choice.

You just passed the LET: here’s how to protect yourself

If you just checked your March 2026 LET results and you are preparing for your first DepEd appointment, the next 90 days are the most financially critical of your career. Lenders know exactly when new teachers enter the system. Here is how to stay ahead of them.

Survive the 90-day payroll gap

Establish a financial air gap first. DepEd’s payroll system takes 60 to 90 days to fully integrate a new appointment. Consequently, you will work full-time for three months without a paycheck. PLI agents and faculty room liaisons target new teachers during this specific window, knowing they need cash before the first salary arrives. Refuse every loan offer until your first official payslip is in your hands. Your salary should be clean before anyone else touches it.

Use GSIS Ginhawa Go for real emergencies. If you genuinely cannot survive the 90-day gap, do not go to a PLI. Instead, the GSIS Ginhawa Go micro-loan program, launched February 2026, offers rates as low as 7% per annum for new government employees. Compare that to the 15% to 22% effective rate on any PLI product. One posted GSIS premium is typically enough to qualify.

Protect your payslip once you are in the system

Know the two-loan cap and enforce it. The 2026 TCAA limits PLI access to two regular APDS deductions per payslip. If you accumulate loans over time and a lender pushes toward a third, cite the TCAA limit and ask your division payroll verifier to confirm what is currently active on your APDS record.

Go to government lenders first, always. Before any PLI, check whether a Pag-IBIG Multi-Purpose Loan or an SSS salary loan covers your need. Government-backed rates are significantly lower, and the difference in total interest paid across a five-year term is substantial.

Ask what MOOE covers before you borrow for equipment. If a school head tells you to comply with a new digital mandate, ask first what the school’s MOOE budget provides for digitalization this year. You are not required to fund government infrastructure with your personal credit line.

When your first clean payslip arrives, that ₱31,705 plus ₱2,000 PERA is real purchasing power. Even redirecting ₱500 a month into a Pag-IBIG MP2 savings account puts you ahead of most colleagues financially. The moment you let a lender touch that payslip before you do, that power is gone.

Frequently asked questions about loans for teachers in the Philippines

What is the minimum net take-home pay for DepEd teachers in the Philippines?

The legal minimum is ₱5,000 per month, mandated under the General Appropriations Act. DepEd’s central payroll software enforces this floor automatically. No new APDS deduction can legally push a teacher below this amount. However, lenders who offer loans for teachers use workarounds such as ATM card pawning and post-dated check coercion to extract money after the payroll floor is technically satisfied.

How many loans can a DepEd teacher have through the APDS?

Under the 2026 TCAA, a DepEd teacher can have a maximum of two regular PLI loans and one calamity loan deducted from their payslip at any time. Before this rule, teachers could accumulate five or more active APDS deductions simultaneously, creating the perpetual ₱5,000 floor situation this post describes.

What happens to loans for teachers if a DepEd teacher resigns?

Most PLI contracts make the full outstanding balance due and demandable immediately upon separation from DepEd service. Without automatic payroll deductions, lenders shift to post-dated check enforcement, BP 22 threats, or administrative complaints. Outstanding GSIS loans can also be offset against terminal leave pay, sometimes reducing a teacher’s final payout to zero.

What is GSIS Ginhawa Go and who can apply?

GSIS Ginhawa Go is a micro-loan program launched in February 2026 for government employees, including DepEd teachers. It offers rates as low as 7% per annum and is designed as a short-term cash bridge. Teachers typically become eligible after their first GSIS premium is posted, making it a significantly safer alternative to any PLI product.

Is teacher debt in the Philippines a financial literacy problem?

No. Loans for teachers exist because the salary is structurally below the cost of living, not because teachers lack financial knowledge. Filipino teachers regularly search for GSIS MPL calculators, loan amortization formulas, and exact bonus release dates to manage their finances precisely. A Teacher I earns ₱31,705 basic pay while the estimated family living wage in urban areas has climbed toward ₱40,000 in 2026. No budgeting seminar closes a monthly gap of nearly ₱8,000.

{kind=link}