MP2 is a 5-year savings program, and the early withdrawal rules are stricter than most members expect. Whether you are facing a financial emergency or reconsidering the commitment, the answer to “can I withdraw MP2 before maturity?” is yes, but the cost depends entirely on your reason. For more guides on managing your MP2 account, browse our complete Pag-IBIG savings guides.

Can you withdraw MP2 savings before the 5-year maturity?

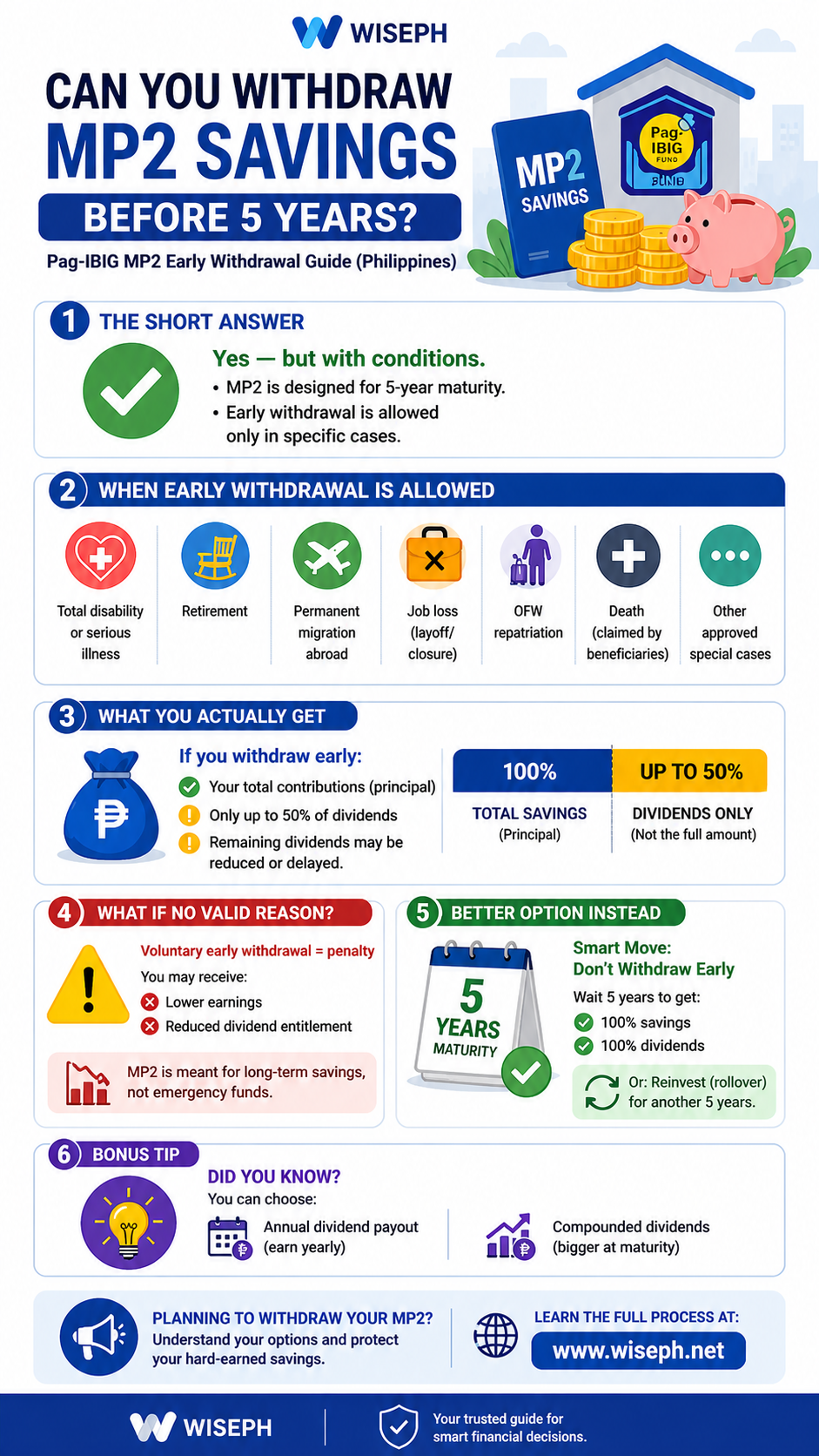

Yes, but only under specific conditions. Outside Pag-IBIG’s approved list of valid reasons, you can still apply for early withdrawal, but you will only receive 50% of the total dividends earned up to that point. Your principal contributions are always returned in full. Early withdrawal is not blocked, but the penalty makes it a costly decision for most members.

Here’s a simple visual breakdown to help you decide:

Quick guide: When you can withdraw MP2 savings early and what you’ll actually receive.

| Situation | Principal | Dividends |

|---|---|---|

| Valid reason (disability, death, retirement, etc.) | 100% returned | 100% released |

| Non-valid reason (voluntary early exit) | 100% returned | Only 50% released |

| Full 5-year term completed | 100% returned | 100% released |

If you are still deciding whether to open an account, the guide on how to open an MP2 account explains the full 5-year program structure before you commit.

What is the penalty for withdrawing MP2 early?

The 50% dividend rule

The penalty for non-valid early withdrawal is 50% of your total dividends earned, not a flat convenience fee. Your principal is safe regardless of the withdrawal reason. Pag-IBIG computes the penalty against all dividends accumulated over the account’s lifetime. This includes everything earned from the start, not just what remains inside the fund today.

Here is what that means in practice. Here is the math in practice. You contributed ₱60,000 over 3 years and earned ₱12,000 in dividends. With the penalty, you receive ₱60,000 in principal plus ₱6,000 (half of dividends), for a total of ₱66,000. Without the penalty, the total would have been ₱72,000. That ₱6,000 gap is permanently forfeited.

Does the penalty grow the longer you wait?

In peso terms, yes. A member who withdraws after 4 years has earned more dividends than someone who withdraws after 1 year. So the 50% cut represents a larger peso amount. The rule is the same; only the earnings base changes.

Use the MP2 savings calculator to see how dividends accumulate at different contribution amounts and time points.

Valid reasons to withdraw MP2 early without penalty

Pag-IBIG officially recognizes 9 grounds for full penalty-free early withdrawal. If your situation falls under any of these, you receive your complete principal and 100% of dividends earned, as if you reached normal maturity.

- Total disability or insanity

- Separation from service by reason of health

- Death of the member or an immediate family member

- Retirement

- Permanent departure from the Philippines

- Unemployment due to layoff or company closure (not voluntary resignation)

- Critical illness of the member or an immediate family member

- Repatriation of an OFW member from the host country

- Other meritorious grounds approved by the Pag-IBIG Board

What counts as critical illness?

Based on Pag-IBIG Fund’s official program terms, critical illness specifically covers cancer, organ failure, heart-related illness, stroke, and neuromuscular-related illness. This applies to both the member and an immediate family member. General illness without a qualifying diagnosis does not meet this threshold. If you are unsure whether a condition qualifies, contact Pag-IBIG Fund directly before submitting a claim.

How to apply for early MP2 withdrawal

Starting the application through Virtual Pag-IBIG

Early withdrawal applications, whether for valid or non-valid reasons, go through the same channel. There is no separate process or form for penalty-free claims. Instead, the reason you select determines the outcome.

- Log in at pagibigfundservices.com

- Go to MP2 Savings on your dashboard

- Select the withdrawal or claim option

- Choose your reason from the available categories

- Upload the required documents (valid ID, claim form, and supporting proof based on your reason)

- Submit and wait for Pag-IBIG’s evaluation and approval

Before applying, verify that your contribution history is accurate and complete. The guide on how to check your MP2 balance and contributions online walks through how to confirm your total contributions and dividend records inside Virtual Pag-IBIG.

What documents are typically required?

The base requirements are a completed claim application form, one valid government ID, and your Pag-IBIG Loyalty Card Plus. For valid-reason claims, you also need supporting proof for your specific situation. This means a medical certificate for disability or critical illness, a death certificate for death-related claims, a separation notice for layoff, or a travel document for permanent departure.

Without the appropriate supporting document, Pag-IBIG processes the claim as a non-valid pre-termination and applies the 50% penalty. For the standard 5-year maturity claim process, the guide on how to claim your MP2 savings covers the full payout steps from maturity date to final disbursement.

Does the penalty change depending on how many years you’ve completed?

No. The 50% dividend penalty is fixed regardless of how far into the 5-year term you are. Pag-IBIG applies the same rule whether you withdraw after 1 year or after 4 years. The percentage does not change; only the peso amount changes because a longer account has accumulated more dividends.

| Years completed | Penalty rate | What changes |

|---|---|---|

| 1 year | 50% of dividends earned | Lower dividend total, smaller peso penalty |

| 3 years | 50% of dividends earned | Larger dividend total, bigger peso penalty |

| 4 years | 50% of dividends earned | Near-full earnings, largest penalty if withdrawn now |

| 5 years (full term) | No penalty | Full payout, no deduction |

This is why withdrawing near the end of the term is still a costly decision. At year 4, you give up half the dividends you spent nearly 5 years building. That full payout would have been yours in just 12 more months.

What if you already received annual dividend payouts?

If you chose the annual dividend payout option and already received dividends for previous years, those past payouts still count. Pag-IBIG includes them in the total dividend computation when you pre-terminate early.

You are not required to physically return the cash already credited to your bank account. However, those amounts factor into the final settlement. As a result, the 50% penalty is not isolated to what remains inside the MP2 fund. It is based on total dividends earned over the entire account life, including payouts you already received.

For example: if you received ₱3,000 in Year 1 dividends and ₱4,000 in Year 2, then pre-terminate in Year 3 without a valid reason, Pag-IBIG factors those past payouts into the penalty computation. The account closure reflects the total, not just the remaining balance inside the fund. This is the detail most members who chose annual payout mode miss when they consider early withdrawal.

What to do instead of withdrawing MP2 early

If your situation does not qualify for penalty-free withdrawal, work through these options before touching your MP2 savings. In most cases, a short-term fix costs less than permanently losing 50% of your MP2 dividends.

| Step | Option | Why |

|---|---|---|

| 1 | Emergency fund | Costs nothing, no dividend loss |

| 2 | Salary advance or short-term loan | Short-term cost, keeps MP2 earnings intact |

| 3 | Pag-IBIG Multi-Purpose Loan (MPL) | Low-interest government loan, does not touch MP2 |

| 4 | Pag-IBIG Calamity Loan (if qualified) | Designed for emergency situations, separate from MP2 |

| 5 | MP2 early withdrawal | Last resort; 50% of total dividends forfeited |

Pag-IBIG’s own loan options

Pag-IBIG members can apply for a Multi-Purpose Loan or Calamity Loan directly through Virtual Pag-IBIG. Specifically, these products are completely separate from your MP2 savings. Borrowing from them has no effect on your MP2 account or dividend accumulation. If the financial need is temporary, a short-term loan costs less than permanently forfeiting half your MP2 earnings.

The mistake most MP2 members make about early withdrawal

The biggest misconception circulating on Facebook groups is that MP2 can be pulled out early anytime, as long as you accept a small loss. That is not how the rules work. Early withdrawal is only allowed for specific valid reasons, and outside those reasons, the penalty is 50% of total dividends earned. It is not a token deduction.

I was in that position myself during a tight financial stretch. Expenses piled up and I started looking at my MP2 balance like it was available money. What stopped me was a simple realization: MP2 is not your emergency fund. If I had pulled it out just because I was stressed, I would have permanently lost half the dividends I had been building for years. The problem I was stressed about? I solved it by tightening my budget and using other savings.

The advice I wish I had read before that moment: only put money into MP2 that you genuinely will not need for 5 years. Keep emergency cash in a separate, liquid account. Contribute what you are comfortable locking away, not your last available peso. For more on choosing the right contribution approach, read the guide on lump sum vs. monthly contribution in MP2.

Frequently asked questions

Can I withdraw my MP2 savings before the 5-year maturity for any reason?

Yes, but if your reason is not on Pag-IBIG’s approved list, you will only receive 50% of your total dividends earned. Your principal is always returned in full. The nine valid reasons include total disability, death, retirement, critical illness, layoff, permanent departure from the Philippines, OFW repatriation, separation from service for health reasons, and other Board-approved grounds.

Do I lose my principal contributions if I withdraw MP2 early?

No. Your principal is always returned in full regardless of the withdrawal reason. The penalty applies only to the dividends you earned over the life of the account, not to the money you put in.

How do I apply for early MP2 withdrawal?

Log in to Virtual Pag-IBIG at pagibigfundservices.com, go to MP2 Savings, and select the claim or withdrawal option. Choose your reason, upload your valid ID and supporting documents, and submit. Pag-IBIG evaluates the reason and determines whether the full payout or the 50% penalty applies. The process is the same for valid and non-valid reasons; the outcome is what differs.

Does the 50% dividend penalty apply if I already received annual dividend payouts?

Yes. Pag-IBIG computes the penalty against your total dividends earned, including past payouts already credited to your bank account. You are not required to return that cash, but those amounts factor into the final settlement computation. The penalty is not isolated to what remains inside the MP2 fund.

What is the best alternative to withdrawing MP2 early?

Work through these in order: use your emergency fund first, then a salary advance or short-term loan, then Pag-IBIG’s Multi-Purpose Loan or Calamity Loan if you qualify. Pre-terminate MP2 only as a last resort. For related guidance, browse the full Pag-IBIG savings guides on WisePH.

{kind=link}