A close relative delivered at a private hospital in early 2026. We thought PhilHealth would cover most of the bill. It did help significantly, but not the way we expected.

PhilHealth maternity coverage is a fixed case-rate deduction, not a full reimbursement of every expense. The hospital applies a set amount before discharge. PhilHealth covers everything within the case rate. Everything outside it (private room markups, doctor’s top-up fees, epidural, non-formulary medicines) stays your responsibility. The final bill can still run high depending on where you deliver and what room you choose.

The April 30, 2026 update changed the numbers substantially. This guide covers the new rates, what they include, the most common billing surprises, and exactly what to prepare before your due date so you are not scrambling at the billing window with a newborn in your arms.

How much does PhilHealth cover for normal delivery in 2026?

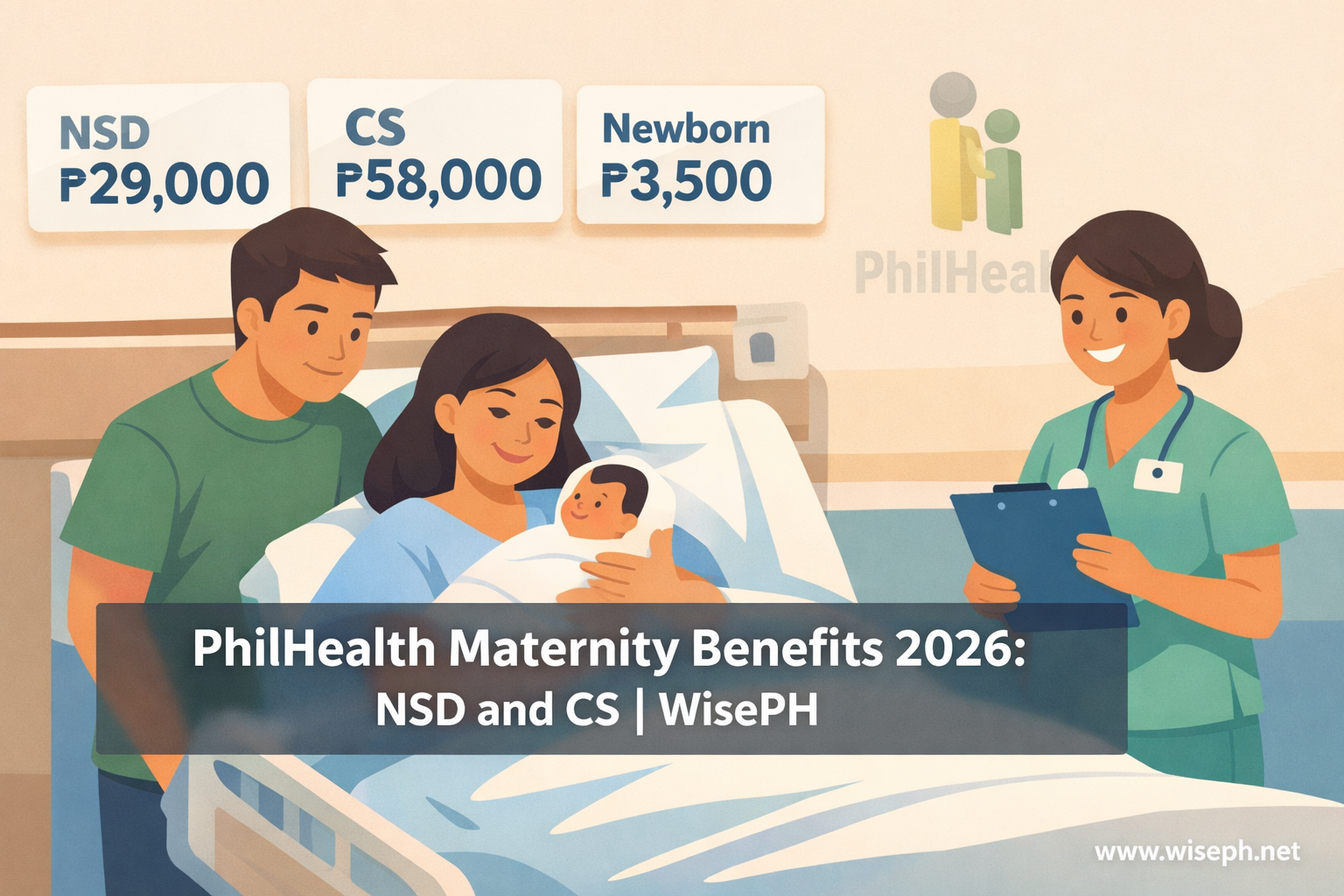

The PhilHealth case rate for a Normal Spontaneous Delivery (NSD) is now ₱29,000, effective April 30, 2026 under PhilHealth Circular No. 2026-0005. That is roughly three times the old rate of ₱9,750.

The ₱29,000 is split: approximately 70% goes to hospital facility charges (room, medicines, supplies, labor monitoring) and 30% to professional fees for the OB-GYN, midwife, and attending pediatrician. The hospital applies the deduction directly to your bill before you settle the balance.

For members delivering in a basic ward at a government or accredited hospital, the No Balance Billing (NBB) policy applies. The hospital cannot charge you more than the PhilHealth case rate for essential delivery services. In a ward at a public hospital, a normal delivery can now realistically result in zero out-of-pocket expenses. Private rooms are a different story, which we cover in a later section.

How much does PhilHealth cover for CS delivery in 2026?

₱58,000 for a primary Cesarean Section. ₱62,000 for a complicated or emergency CS, including cases where a planned normal delivery becomes an emergency C-section during labor. Both rates took effect April 30, 2026, up from the old ₱37,050 for all CS types.

The ₱62,000 tier specifically covers “caesarean delivery following attempted vaginal birth.” If you go into the delivery room expecting an NSD but the doctor calls for emergency surgery due to fetal distress or prolonged labor, the billing department updates your claim code to the complicated CS tier and applies the higher deduction. You do not get charged for both an NSD attempt and a CS.

| Delivery type | 2026 case rate | Previous rate |

|---|---|---|

| Normal Spontaneous Delivery (NSD) | ₱29,000 | ₱9,750 |

| Primary Cesarean Section | ₱58,000 | ₱37,050 |

| Complicated / Emergency CS | ₱62,000 | ₱37,050 |

What prenatal care does PhilHealth cover?

PhilHealth now covers a minimum of 8 prenatal checkups, up from 4. Each visit can include essential laboratory tests (CBC, urinalysis, blood typing) and maternal vaccines such as Tetanus Toxoid. The subsidy ranges from ₱1,500 to ₱3,750 per complete prenatal package, depending on the type of facility.

The biggest change in 2026 is that prenatal care is now an independent outpatient benefit, no longer bundled into your delivery bill. This means you can have all your checkups at a local clinic and deliver at a different hospital, and you can still claim the prenatal subsidy separately. Previously, switching facilities often meant losing part of the benefit.

To claim the prenatal subsidy, the billing office needs documented proof of those 8 visits. Your Mother’s Book (the maternal health record issued by your prenatal clinic) must have the attending doctor or midwife’s signature and date for each visit. Missing entries can cause the billing department to reject the prenatal portion of your claim, even if you attended every appointment.

After delivery, PhilHealth also covers 3 postnatal follow-up visits: within 72 hours of discharge, within 7 days, and within 4 to 6 weeks. The final visit includes postpartum family planning counseling. If you choose a long-term contraceptive method (IUD, implant) during that window, PhilHealth may cover it under a separate family planning case rate.

What does PhilHealth cover for the newborn?

From birth, your baby is a separate PhilHealth patient with a separate bill. The hospital deducts the ₱3,500 Newborn Care Package (NCP) from the baby’s bill, not from your ₱29,000 or ₱58,000 maternity case rate. Both bills are independent.

This package covers newborn screening, hearing screening, Hepatitis B vaccine (first dose), BCG vaccine, Vitamin K administration, eye ointment prophylaxis, and the attending pediatrician’s professional fee for the delivery room assessment.

To trigger the NCP deduction, the hospital must process the baby as a separate PhilHealth claimant. Before discharge, accomplish the PMRF (PhilHealth Member Registration Form) to register the newborn as your dependent. Skip that step and the hospital may not apply the ₱3,500 deduction. See the full guide on who qualifies as a PhilHealth dependent for registration rules.

If the baby arrives early or needs intensive care, Z Benefits for premature and small newborns replace the NCP:

- Highly premature (under 32 weeks gestation or under 1,500g): ₱35,000 to ₱135,000

- Moderately premature (32 to under 37 weeks, 1,500g to 2,500g): ₱24,000 to ₱71,000

Z Benefits are only available at PhilHealth-contracted hospitals, typically major government tertiary centers and specialized regional hospitals. If you are high-risk, ask your OB during the third trimester whether your delivery hospital is contracted for Z Benefits. A non-contracted private hospital applies only standard sick-newborn case rates, which are far lower.

How many contributions do you need to qualify?

The requirement is 9 months of paid contributions within the 12-month period immediately before your delivery month. This is the 9/12 rule. If you deliver in December 2026, PhilHealth checks contributions from December 2025 to November 2026. At least 9 of those 12 months must be paid.

The most common mistake: trying to pay missing months on the day of admission. The hospital’s real-time eligibility system (HCI Portal) checks your status at admission. A payment made that morning usually hasn’t been processed yet, so your status still shows as ineligible. Settle any gaps at least one full month before your due date.

If you discover gaps while already pregnant, self-employed and voluntary members can take advantage of the 2026 One-Time Interest Waiver (PhilHealth Circular No. 2026-001), which allows missed contributions to be paid without penalties until December 31, 2026. Pay the principal only, advance the remaining months, and your 9/12 count improves without the usual surcharges.

If you are close to your due date and genuinely cannot cover the missed months, ask the hospital’s Medical Social Worker (MSW) about Point of Service (POS) enrollment. The MSW can assess your situation and, if you qualify as financially incapable, enroll you as a sponsored member on the spot for immediate coverage. To check your current contribution status, see the guide on how to check your PhilHealth contributions online.

The out-of-pocket expenses that catch families off guard

Four surprises show up most often at the billing window.

Professional fee top-ups. PhilHealth allocates roughly 30% of the case rate for doctors’ fees. In private hospitals, OB-GYN and anesthesiologist rates routinely exceed that allocation. If your doctor’s fee is ₱25,000 and PhilHealth’s portion covers ₱15,000, you pay the ₱10,000 difference. Ask for a professional fee estimate during your 7th or 8th month, not on delivery day.

The private room price multiplier. PhilHealth deducts the same ₱29,000 to ₱62,000 regardless of your room. But in a private room, hospitals often charge 20 to 50 percent more for medicines, supplies, and lab tests compared to ward prices. The case rate doesn’t expand to match. You absorb the markup on everything. The No Balance Billing protection only applies to basic ward accommodations.

Supplies and admission kits. Maternity pads, diapers, alcohol, cotton, and the standard “admission kit” are billed at hospital pharmacy rates. Most hospitals let you bring your own supply bag. Ask for their required items list during the third trimester and buy everything at a supermarket before you go in.

Epidural and non-routine add-ons. An epidural is generally not part of the NSD or CS case rate. The anesthesiologist’s fee for pain management and the specialized medication are billed separately. Extended stays beyond the standard 3 to 4 days for a CS are also fully out of pocket if the extra days are for convenience rather than medical necessity.

For freelancers, self-employed members, and OFWs

The core difference: no HR officer to sign your paperwork. Employed members have Part II of Claim Form 1 (CF1) signed by an HR officer certifying that contributions were deducted. Freelancers and self-employed members don’t have that. Eligibility runs entirely through the PhilHealth portal.

When the hospital generates your PhilHealth Benefit Eligibility Form (PBEF), if it shows “Eligible,” no receipts are needed. If it shows “Not Eligible” (due to a system lag, a missed month, or a mismatched membership category), you need to show your payment records: GCash or Maya payment screenshots, portal payment confirmations, or Official Receipts. Keep 12 months of receipts in a folder on your phone before your third trimester ends.

Update your membership category before admission. If you were previously employed but are now freelancing, make sure the system reflects “Self-Earning Individual.” A mismatched category causes the hospital portal to look for an employer signature that doesn’t exist, which delays your discharge. For a full breakdown of membership rules by category, see PhilHealth rules for self-employed, voluntary, and senior members.

OFWs delivering in the Philippines follow the same process as local freelancers. OFWs who deliver abroad have 180 days from the date of discharge to file a reimbursement claim at a PhilHealth office in the Philippines or at the relevant Philippine Embassy or Consulate.

What to prepare before your due date

Do these five things by your 36th week. Waiting until labor starts is too late for most of them.

- Check your portal status. Log in to the PhilHealth Member Portal and verify that your eligibility shows “Active” with at least 9 paid months in the last 12. If you have gaps, settle them immediately and use the 2026 interest waiver if applicable.

- Ask your OB for a professional fee estimate. Get a specific peso figure for your OB-GYN and, if relevant, the anesthesiologist. Ask whether their fee is within the PhilHealth case rate or if there will be a top-up.

- Prepare your physical backup folder. Have a printed or clearly photographed copy of your MDR, your last 12 months of contribution receipts, and your prenatal records. The guide on how to download your PhilHealth MDR covers that step. The complete PhilHealth claims documents list covers what else to bring.

- Prepare the PMRF for your baby. Have a blank or pre-filled PhilHealth Member Registration Form ready to accomplish at the hospital. The baby’s ₱3,500 NCP deduction requires the newborn to be registered as your dependent before discharge.

- Ask the hospital one practical question. Visit the hospital billing section during a routine prenatal visit and ask: “Do you use the real-time PBEF system, or do I need to bring a printed Certificate of Contribution?” Smaller clinics sometimes still require the paper certificate. Know in advance so you are not surprised on delivery day.

Frequently asked questions

How much is the PhilHealth maternity benefit for normal delivery in 2026?

The PhilHealth case rate for Normal Spontaneous Delivery (NSD) is ₱29,000 as of April 30, 2026, under Circular No. 2026-0005. That is roughly three times the previous rate of ₱9,750. The hospital applies this as a fixed deduction before you settle the balance. Members delivering in a basic ward at an accredited hospital are protected by No Balance Billing.

Is the baby’s Newborn Care Package separate from the mother’s case rate?

Yes. Your baby is a separate PhilHealth patient from birth. The ₱3,500 Newborn Care Package (NCP) comes from the baby’s bill, not from your ₱29,000 or ₱58,000 maternity case rate. You must accomplish a PMRF to register the baby as your dependent before leaving the hospital so the deduction is applied correctly.

What is the 9/12 rule for PhilHealth maternity?

You need at least 9 months of paid contributions within the 12-month period before your delivery month. Do not pay missing months on the day of admission. The real-time hospital portal takes time to reflect new payments, so a same-day payment usually will not update your eligibility status in time. Settle gaps at least one month before your due date.

Can I use PhilHealth maternity benefits at a private hospital?

Yes, at any PhilHealth-accredited hospital. The case rate deduction applies whether the facility is public or private. No Balance Billing protection only covers basic ward accommodations, though. In a private room, higher medicine prices, supply markups, and professional fee top-ups can significantly increase your out-of-pocket share.

What if my planned normal delivery becomes an emergency CS?

PhilHealth covers this at the ₱62,000 complicated CS rate. Once the emergency surgery happens, the hospital updates your claim code. You are not charged for an NSD attempt and a separate CS. The ₱62,000 deduction is applied to your final bill, specifically designed to absorb the added operating room and anesthesiologist costs from the unplanned procedure.

Browse the complete PhilHealth guides on WisePH for step-by-step help on contributions, benefits, eligibility, and claims.

While you prepare for your growing family, it is also a good time to review your long-term savings. The Pag-IBIG MP2 savings account earns tax-free dividends and is open to any Pag-IBIG member, including self-employed contributors and OFWs.

{kind=link}