I get this Viber call more often than I can count. A colleague here in Dubai, voice tight with stress: “Kuya, ang laki ng bill! Akala ko covered na ng PhilHealth lahat!” Then we open the hospital statement together over the phone, line by line.

The pattern is almost always the same. They chose a private or semi-private room. “Mas comfortable para sa mama,” they said. And then the bill came.

I am a hospital professional based in Dubai. From here, I review and coordinate PhilHealth claims for OFW colleagues whose families are admitted to hospitals back home. This guide covers exactly what I tell them before the admission happens, not after. For a broader look at PhilHealth eligibility rules, read our guide on how to check if you are eligible for PhilHealth benefits first.

How PhilHealth actually pays your hospital bill

PhilHealth does not reimburse you. It pays a fixed case rate directly to the hospital, and the hospital deducts that amount from your bill. You pay whatever is left.

This is the most misunderstood fact about the entire system. Most Filipinos think PhilHealth sends money back to them after they pay the full bill. In reality, however, the hospital files the claim and PhilHealth wires the payment straight to the hospital’s account. You never see that money. You only see a smaller final bill.

The case rate is a fixed all-in package. It covers room and board (ward level only), medicines listed in the package, basic laboratory tests, doctor’s professional fees, and operating or delivery room fees. What it does NOT cover is everything else: room upgrades, medicines outside the formulary, extra tests beyond the package, and non-medical charges.

What is No Balance Billing, and where does it stop protecting you?

No Balance Billing (NBB) means the hospital cannot charge you anything above what PhilHealth pays for the covered services. In a basic ward room, you walk out paying close to zero for everything the package covers. The hospital absorbs the difference between PhilHealth’s payment and their actual costs. They cannot pass that gap on to you.

Under the 2026 rules, NBB applies to all PhilHealth members and qualified PhilHealth dependents admitted to basic or ward accommodation in accredited public and private hospitals. The new maternity circular PC2026-0005 strengthened this for all deliveries in ward.

What NBB covers in ward

- Room and board at ward level

- Medicines and supplies listed in the PhilHealth package

- Basic laboratory tests and procedures

- Doctor’s professional fees for the covered case

- Operating or delivery room fees

- Salaried nursing staff services

Where NBB stops protecting you

The moment you choose a private or semi-private room, NBB disappears entirely. The hospital is legally allowed to charge the full difference in room rate, better meals, private bathroom, air conditioning, television, extra nursing attention, and everything else that comes with upgraded accommodation. The case rate stays the same regardless of room type. Your out-of-pocket is the only thing that changes.

NBB also does not cover medicines outside the official PhilHealth formulary, tests or procedures ordered beyond the package, complications not listed in the protocol, or any services from specialists not included in the case rate. As a result, families often still get billed for branded antibiotics, extra scans, or certain newborn services even in a ward room.

Government hospital vs. private hospital: the real coverage difference

The PhilHealth case rates are the same whether you are in a government or private hospital. A ₱29,000 NSD case rate pays ₱29,000 to either facility. In practice, however, the out-of-pocket experience is very different.

Government and public hospitals

In a basic ward room at a DOH, provincial, or LGU-run hospital, PhilHealth’s fixed payment plus the government subsidy usually covers the full cost of your ward stay, formulary medicines, labs, and procedures. Many public hospitals now offer expanded zero-balance billing for PhilHealth members in their pay wards as well, as of 2026 updates. The Malasakit Center, present in many DOH hospitals, can also cover remaining gaps using additional government funds. For catastrophic cases like Z Benefit for cancer or kidney transplant, public hospitals are where the financial protection is strongest. Read the full guide to the PhilHealth Z Benefit package for those cases.

However, the tradeoff is real: crowded wards, longer wait times, older equipment, and the occasional need to bring your own supplies during peak periods.

Private hospitals

In ward accommodation at a private hospital, NBB now applies strongly under the 2026 rules, especially for maternity. Mothers delivering in ward are walking out with zero or very low out-of-pocket for the PhilHealth-covered delivery package. See the complete guide to PhilHealth maternity benefits 2026 for exact amounts.

For non-maternity cases, private hospitals in ward still provide good protection. However, there is a higher chance of small extras outside the formulary. The bigger risk is the private room upgrade. Most families choose it for comfort, and that single decision is where the large surprise bills come from. Similarly, private hospitals are more likely to stock and use branded medicines or newer tests that fall outside the PhilHealth package.

PhilHealth case rates for the most common hospitalizations in 2026

These are the fixed amounts PhilHealth pays to the hospital for each condition. They do not increase if you choose a private room. Therefore, understanding these numbers before admission tells you exactly what PhilHealth will absorb. For exact rates by severity, use the official PhilHealth case rates search tool and enter the specific diagnosis.

| Condition | PhilHealth case rate (approx.) | What it covers in ward |

|---|---|---|

| Normal spontaneous delivery (NSD) | ₱29,000 | Delivery, basic newborn care, prenatal and postnatal packages |

| Cesarean section (primary or repeat) | ₱58,000 to ₱62,000 | Surgery, anesthesia, recovery, basic newborn care |

| Pneumonia (moderate risk) | ₱15,000 to ₱29,250 | IV antibiotics, oxygen, room, basic labs |

| Pneumonia (high risk or severe) | ₱32,000 to ₱90,100 | Higher-level care, possible ICU classification |

| Hemorrhagic stroke | ₱38,000 | Acute care, CT scan, basic rehab support |

| Acute myocardial infarction (heart attack) | ₱36,000 | ECG, basic cardiac monitoring, medicines |

| Dengue hemorrhagic fever | ₱16,000 | IV fluids, platelet monitoring, room |

| Dengue fever (simple) | ₱10,000 | Hydration, observation, basic labs |

| Urinary tract infection | ₱6,500 to ₱9,000 | Antibiotics, urinalysis, culture |

| Hypertension / hypertensive emergency | ₱12,285 to ₱17,550 | BP management, monitoring, basic labs |

For catastrophic cases like cancer, kidney transplant, or heart surgery, however, the Z Benefit packages apply; these are separate from regular case rates and require pre-authorization at a contracted Z facility. If your family member has lapsed PhilHealth contributions, those must also be cleared before these packages can be accessed.

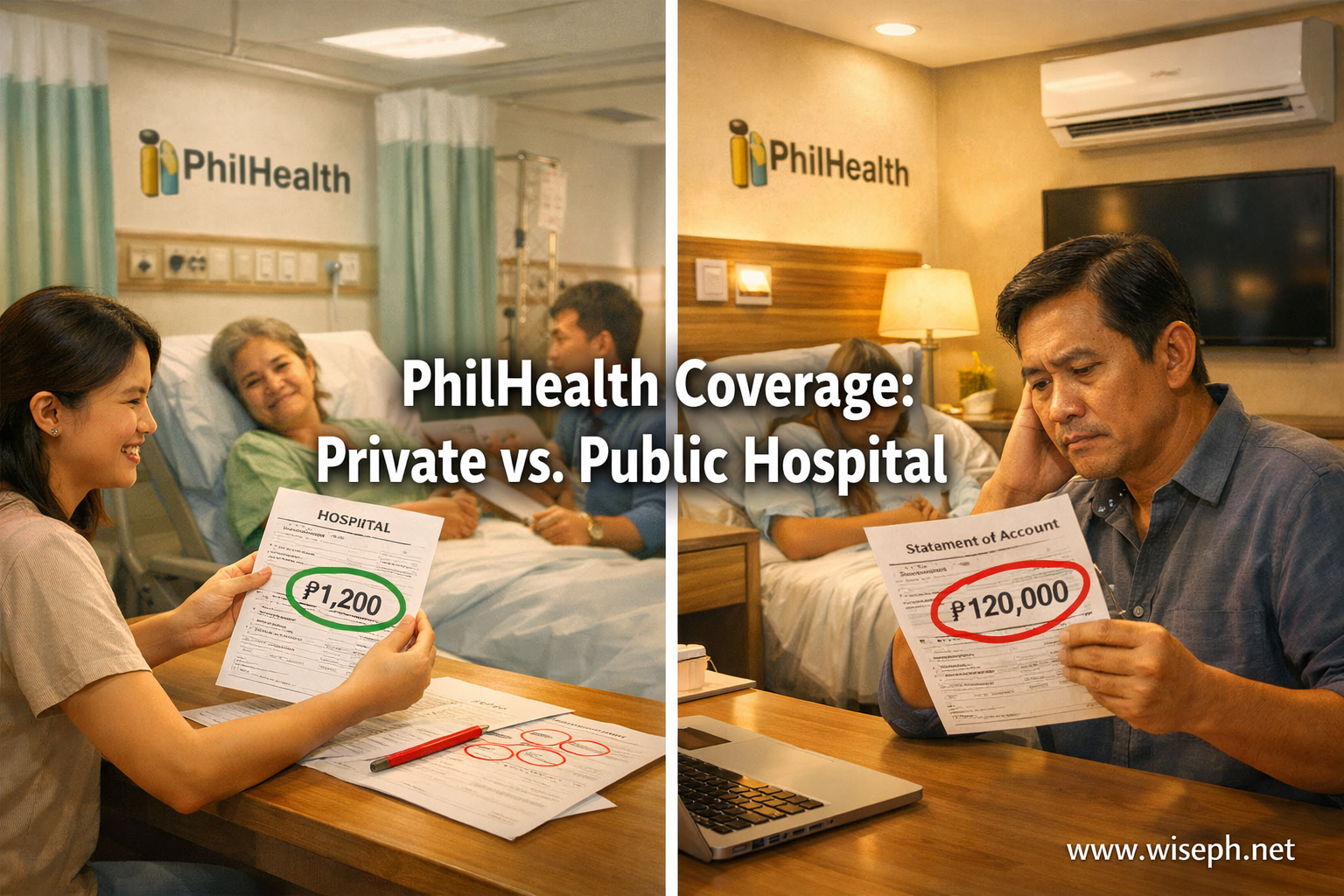

The same pneumonia treatment, two different bills

A 35-year-old woman, admitted for moderate pneumonia in a Level 2 private hospital in the province, June 2026. Five days of stay, the same IV antibiotics, the same labs, the same doctor. The only difference was room choice, and it cost one family ₱105,300 more than the other.

Family A: ward accommodation (No Balance Billing applies)

| Item | Amount |

|---|---|

| Total hospital bill before PhilHealth | ₱68,000 |

| PhilHealth case rate paid to hospital | ₱28,500 |

| Small extras outside formulary (paracetamol, one branded nebulizer ampule) | ₱4,200 |

| Final amount Family A paid | ₱4,200 |

They walked out almost stress-free. The PhilHealth case rate plus the NBB policy absorbed almost everything covered under the package. That is the system working exactly as it should.

Family B: private room (NBB does NOT apply)

| Item | Amount |

|---|---|

| Total hospital bill before PhilHealth | ₱138,000 |

| PhilHealth case rate paid to hospital | ₱28,500 |

| Private room gap (₱4,000/night x 5 days + meals + extras) | ₱109,500 |

| Final amount Family B paid | ₱109,500 |

They were in shock. “May PhilHealth naman,” but the case rate did not grow with the room upgrade. PhilHealth still paid its fixed ₱28,500. The hospital charged Family B the full difference in room rate, meals, and amenities. Same treatment, same hospital, same doctor. In contrast, Family A paid ₱4,200. That is a ₱105,300 difference for the exact same illness.

When a private room is actually worth the extra cost

I do not always say no to a private room. Sometimes the extra money is worth it, but only in specific situations. These are the cases where I tell OFW colleagues to pay the gap.

- Post-CS recovery, especially for first-time moms. Pain, limited mobility, and the need for frequent monitoring make a private room worth it. Moms in ward after a CS often struggle with noise, shared bathrooms, and limited space for the baby. One colleague’s wife chose a private room for her CS recovery (₱55,000 extra). As a result, she recovered faster, breastfed better, and had less postpartum anxiety. He said it was worth every peso.

- Elderly patients (60 and above). Seniors get confused in noisy wards, have higher fall risk, and often do better with a quieter environment. Privacy also helps with dignity during recovery.

- Long hospital stays (5 or more days). For stroke recovery, complicated pneumonia, or heart failure, the mental toll of a crowded ward grows fast. Better sleep generally means faster recovery.

- Patients with anxiety or mental health conditions. Shared rooms with crying babies, loud visitors, or very sick roommates can make anxiety noticeably worse.

- The OFW family can genuinely afford the gap. If the fund is there and peace of mind matters more than the savings, that is a valid choice.

Ward is also the right call for short stays (2 to 4 days), young and otherwise healthy patients, simple cases like uncomplicated NSD, mild pneumonia, UTI, or dengue without complications, and tight budgets with no emergency fund. In those situations, the savings are real and the medical difference is minimal. Before committing, ask the attending doctor directly: “Doc, medically speaking, is there any reason my family member cannot stay in ward?” If the doctor says either is fine, go ward.

What if the hospital is not PhilHealth-accredited?

In a genuine emergency, go to the nearest hospital first. Do not risk a patient’s life chasing accreditation. Stabilize, then transfer to an accredited facility if the patient can safely be moved. You can still recover part of your PhilHealth benefit after that.

Emergency admissions in non-accredited hospitals

PhilHealth allows direct reimbursement for emergency confinements in non-accredited hospitals and for situations where the nearest accredited facility is too far. In this case, you (or your family) file the claim yourselves instead of letting the hospital do it. The window is 60 days from discharge to file at any PhilHealth Local Health Insurance Office (LHIO) or regional office. OFWs returning from abroad have 180 days.

How to file the reimbursement

Gather the following before going to the LHIO: PhilHealth Claim Forms 1 and 2, official receipts and itemized Statement of Account, discharge summary or clinical abstract, PhilHealth ID or MDR, and a doctor’s certification of emergency. The complete PhilHealth claim documents checklist has the full list. In practice, families in this situation recover 30 to 70 percent of the standard case rate, and processing takes 30 to 90 days.

For voluntary or senior citizen members, the same reimbursement rules apply. However, if contributions have recently lapsed, those need to be cleared first before a claim can proceed. Know the accredited hospitals near your family before an emergency happens. You can check the latest list at philhealth.gov.ph under Accredited Health Facilities, or visit the PhilHealth contracted health facilities page.

Five things to confirm with the hospital before admission

I give this checklist to every OFW colleague planning a procedure or delivery for their family back home. Do this at least one to two weeks before admission day.

The pre-admission checklist

- Confirm the hospital is PhilHealth-accredited for the specific case rate. Ask: “Is this hospital fully accredited for the [specific condition] case rate?” Some hospitals are accredited but not for every package. Also ask for the exact case rate amount for the diagnosis.

- Get two separate written quotations. This is the most important step. Ask the Billing or PhilHealth officer for: Quotation 1 (ward with full PhilHealth and No Balance Billing) and Quotation 2 (private room with estimated out-of-pocket gap). The difference is often ₱40,000 to ₱150,000+. Request both in writing via email or printed form.

- Ask about required documents and confirm a PBEF check. Confirm they need your latest PhilHealth MDR and valid IDs. Ask them to run a PBEF (PhilHealth Benefit Eligibility Form) check before admission to confirm your eligibility shows “Yes.” If the PBEF returns “No” due to contribution issues, read the guide on what happens if PhilHealth contributions lapse before admission day.

- Ask specifically what is NOT covered. Which medicines or labs fall outside the package? Will there be extra professional fees? For delivery cases: are baby vaccines or circumcision covered? Is a deposit required even with PhilHealth?

- Get the direct contact of the hospital’s PhilHealth officer. Ask for their name and mobile number. Tell them: “My family member is an OFW-dependent. We want to maximize coverage. Can we speak before admission?” A five-minute call before admission can save a family ₱50,000 to ₱100,000 at discharge.

Meanwhile, the PhilHealth YAKAP program also covers outpatient primary care and basic medicines through registered clinics, which can reduce the number of cases that escalate to costly hospitalizations. If your family member has not registered yet, read the PhilHealth YAKAP program guide to find an accredited provider near them.

Frequently asked questions about PhilHealth hospital coverage

Does PhilHealth pay me or the hospital directly?

PhilHealth pays the hospital directly. It wires a fixed case rate to the hospital’s account once the claim is approved, and the hospital deducts that from your bill. You pay whatever is left. In almost all cases, you will never receive money directly from PhilHealth.

What is No Balance Billing and who qualifies?

No Balance Billing means the hospital cannot charge you anything above what PhilHealth pays for covered services. It applies to all PhilHealth members and dependents in basic ward accommodation at accredited hospitals. The coverage includes the room, formulary medicines, lab tests, doctor’s fees, and operating room fees. However, it does not apply if you choose a private or semi-private room.

Why is my hospital bill still high even with PhilHealth?

Almost always: a private room upgrade. No Balance Billing only applies in ward. If the family chose a private room, consequently, the hospital charges the full room difference on top of the fixed case rate. Other reasons include medicines outside the formulary, extra lab tests, and procedures beyond the approved package.

Is PhilHealth coverage the same in government and private hospitals?

The case rate is the same in both. However, government hospitals provide stronger real-world protection because the government subsidy fills gaps that private hospitals pass to patients. In government wards, most members pay close to zero. In private hospital wards, NBB applies but small extras are more common. Private rooms anywhere remove NBB protection entirely.

What if I was admitted to a non-PhilHealth-accredited hospital?

Go to the nearest hospital first in a true emergency. After discharge, file a direct reimbursement claim at any PhilHealth LHIO within 60 days (180 days for OFWs returning from abroad). Bring official receipts, an itemized statement of account, discharge summary, PhilHealth ID or MDR, and a doctor’s emergency certification. Families typically recover 30 to 70 percent of the standard case rate this way.

The two-quotation rule saves families from the biggest shock in Philippine healthcare: choosing a private room and assuming PhilHealth’s case rate will cover most of it. Ask for both estimates before anyone signs an admission form. That five-minute conversation is the most valuable thing I tell every OFW colleague from 7,000 km away. For all PhilHealth guides in one place, visit our PhilHealth coverage and benefits section.

{kind=link}